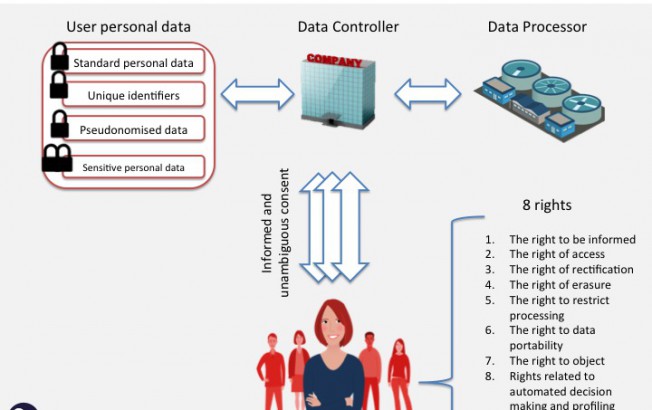

The open banking framework was published this week by the open banking working group. Here I share my 10 most salient take outs in 10 slides. Before we start, I think they have done a tremendous job. It’s an excellent document, the proposals are bold, well presented and discussed. The work is definitely not over, but it’s indeed promising and it should have a material impact on legislations like PSD2. I do think that they are on the right path to meet their mission statement: Unlocking the potential of open banking to improve competition, efficiency and stimulate innovation Here are my key takeouts in 10 slides: 1 -Data, API, Security 2 – A 3 party model 3 – Data: portable, explicit consent and specific usage 4 – A rich variety of data sets 5- Data sets: more granular details 6 – Example: 6 potential propositions enabled by…